The One17 halal fund (Nigeria) — what it is

An educational overview of One17’s Shariah-compliant mutual fund: asset types, common Islamic contracts, fees, allocation ranges, and how to subscribe.

A SEC-regulated, Shariah-compliant mutual fund is a serious product — read the prospectus, factsheet, and Shariah board materials on the manager’s site before investing. This article is not an offer or recommendation.

What is the One17 halal fund?

The One17 halal fund is an open-ended mutual fund managed by One17 Capital Limited. The idea is to pool money into a diversified portfolio that avoids riba and non-compliant sectors (e.g. alcohol, gambling), subject to their stated investment policy and Nigerian regulation.

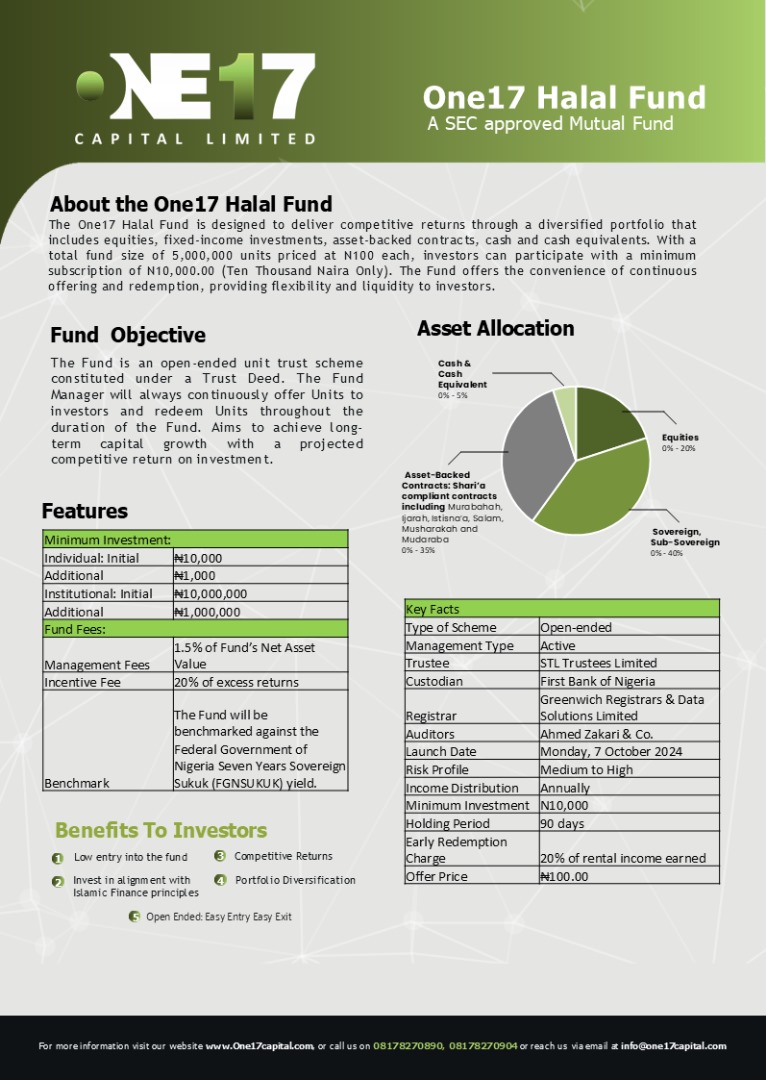

What the fund may invest in (conceptual buckets)

| Type | Meaning | Example |

|---|---|---|

| Equities | Shares in screened companies | Halal-listed names, subject to financial ratios |

| Fixed income (Islamic) | Non-interest income, often via Sukuk | Sovereign or corporate Sukuk, as permitted |

| Asset-backed contracts | Real-economy, contract-based cash flows | Murabaha, ijarah, etc. (see below) |

| Cash equivalents | Short-term liquidity sleeve (often small %) | For redemptions and operations |

Asset-backed contracts (simple glossary)

1. Murabaha (cost-plus sale)

The fund buys an asset and sells it onward at an agreed marked-up price, with payment deferred — profit is known upfront, but the structure is sale-based, not a riba loan. (Scholars and auditors still review how it is implemented.)

2. Ijarah (lease)

The fund buys an asset and leases it for rent.

3. Istisna (manufacturing / construction)

Paying a manufacturer to deliver an asset later; the fund’s role is structured as production finance, not a simple interest loan.

4. Salam (forward purchase)

Paying upfront for future delivery of goods (common in agricultural supply chains in classical fiqh examples).

5. Mudarabah (profit-sharing)

Capital from investors + work from an entrepreneur; profits are shared by agreement; losses follow the rules of the contract (often borne by capital unless misconduct).

Fees (as described in public materials — verify current)

Management fee

1.5% of NAV per year (example from materials).

If your holding is worth ₦500,000 → 1.5% ≈ ₦7,500/year before other costs (check how it is accrued in the prospectus).

Incentive fee

20% of excess returns vs a stated benchmark (e.g. FGN Sukuk yield in their materials).

Example sketch:

- Benchmark return: 10%

- Fund return: 15%

- Excess: 5% → on ₦500,000, excess profit ≈ ₦25,000 → incentive ≈ 20% of that = ₦5,000

Always use the official fee table in the latest prospectus.

Indicative allocation ranges (from notes — confirm live)

| Sleeve | Range (indicative) |

|---|---|

| Sovereign / sub-sovereign Sukuk | 50–60% |

| Halal equities | ~20% |

| Asset-backed contracts | 20–35% |

| Cash & equivalents | 0–5% |

How to subscribe (starting points)

- Website: one17capital.com/halal-mutual-fund

- Short link (as shared publicly): tinyurl.com/Halalfund

- Phone / WhatsApp (from materials): 090647378078

You will typically complete KYC, sign subscription forms, and transfer the minimum investment.

Minimums (from materials)

| Investor | Initial | Additional |

|---|---|---|

| Individual | ₦10,000 | ₦1,000 |

| Institutional | ₦10M | ₦1M |

Monitoring your investment

- Fund reports and NAV updates

- Online dashboard (if offered)

- Compare to the benchmark disclosed in documents

Monthly saving ideas (illustrative)

| Goal | Suggested monthly amount |

|---|---|

| Emergency fund | ₦10,000 – ₦20,000 |

| Hajj / Umrah | ₦15,000 – ₦30,000 |

| Education | ₦10,000 – ₦25,000 |

| Retirement | ₦20,000 – ₦50,000+ |

Tags

Enjoyed this?

Get notified when I publish new articles. No spam, unsubscribe anytime.

Or follow via RSS